StudentShare

Our website is a unique platform where students can share their papers in a matter of giving an example of the work to be done. If you find papers

matching your topic, you may use them only as an example of work. This is 100% legal. You may not submit downloaded papers as your own, that is cheating. Also you

should remember, that this work was alredy submitted once by a student who originally wrote it.

✕

Free

Accounting Systems in Healthcare - Essay Example

Summary

The essay "Accounting Systems in Healthcare" focuses on the discussion of various accounting systems used for managing expenses and also describes future works of the accounting systems in the healthcare segment. The healthcare segment is a rapidly growing segment in the US economy…

- Subject: Health Sciences & Medicine

- Type: Essay

- Level: Undergraduate

- Pages: 5 (1250 words)

- Downloads: 0

- Author: jordonnitzsche

Extract of sample "Accounting Systems in Healthcare"

Accounting Systems in Health care Accounting Systems in Health care Thesis ment: The aim of the essay is to undertake a study on accounting system and how it has been implicated in the healthcare segment. The essay discusses various accounting systems used for the purpose of managing expenses and also describes future works of accounting system in the healthcare segment.

I. Introduction

The healthcare segment is regarded as a rapidly growing segment in the United States economy. This industry concentrates on prevention, analysis, treatment and therapy of wound and disease. The demand of most of the healthcare services is dependent on the requirement of people rather than desire. While the demand of healthcare services is sporadic, the requirement is immediate in nature. This unique characteristic of healthcare segment necessitates most hospitals to maintain a constant access to emergency services and to manage risk, finance and administration. Owing to the constant growth of healthcare industry, it becomes a challenge to heighten the operational effectiveness. Management accountants who perform for healthcare service providers face difficulties in monitoring billing and collection procedure. Thus, a proper accounting system can lead to the attainment of higher operational effectiveness in the healthcare industry (Langabeer et al., 2010).

II. Background

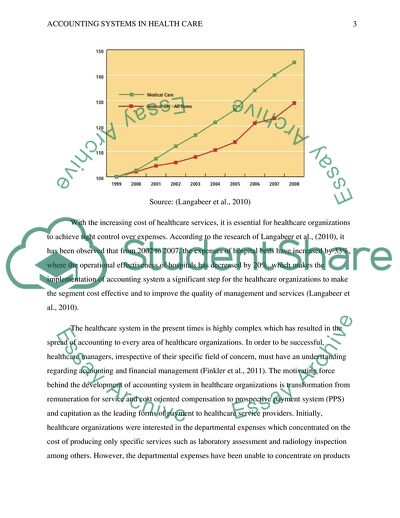

From 1990s, the healthcare environment has emphasized managed care, where the effort of managers in healthcare organizations was directed towards the minimization of expenses and the maintenance of quality of services. In the healthcare segment, the annual expenses have increased considerably and one of the key reasons for this increasing cost is a lack of accounting system in this segment (Toso, n.d.). The following figure demonstrates the increasing trend of cost in the healthcare segment in the US.

Source: (Langabeer et al., 2010)

With the increasing cost of healthcare services, it is essential for healthcare organizations to achieve tight control over expenses. According to the research of Langabeer et al., (2010), it has been observed that from 2002 to 2007, the expenses of hospital beds have increased by 33%, where the operational effectiveness of hospitals has decreased by 20%, which makes the implementation of accounting system a significant step for the healthcare organizations to make the segment cost effective and to improve the quality of management and services (Langabeer et al., 2010).

The healthcare system in the present times is highly complex which has resulted in the spread of accounting to every area of healthcare organizations. In order to be successful, healthcare managers, irrespective of their specific field of concern, must have an understanding regarding accounting and financial management (Finkler et al., 2011). The motivating force behind the development of accounting system in healthcare organizations is transformation from remuneration for service and cost oriented compensation to prospective payment system (PPS) and capitation as the leading forms of payment to healthcare service providers. Initially, healthcare organizations were interested in the departmental expenses which concentrated on the cost of producing only specific services such as laboratory assessment and radiology inspection among others. However, the departmental expenses have been unable to concentrate on products being manufactured by the hospitals and healthcare services delivered to the patients. Thus, the concept of ‘Diagnostic Related Groups’ (DRG) appeared in accounting system of healthcare segment in order to evaluate the course of cost for different products and services. The improvement that has occurred in the healthcare segment is ‘product line costing’, the key purpose of which is to make the payment and reimbursement system convenient and to make the operations effective (Toso, n.d.).

III. Current Practices and Argument

There are several current practices in the area of accounting system in healthcare such as product line costing, job order costing, process costing and standard costing.

Product Line Costing: In product line costing, the relationship between products’ price and costs is recognized in order to understand the financial influence of different types of patients on healthcare organizations. Product line costing focuses on accruing different costs and allocating them to products or services (Toso, n.d.).

Job Order Costing: Job order costing is utilized directly to allocate expenses to patients that consume diverse extents of resources. It averages the expenses on small number of patients. Job order costing necessitates comprehensive information to be recalled and generates more precise cost information for healthcare organizations (Toso, n.d.).

Process Costing: Process costing is implemented for assigning expenses to patients that consume almost the similar extent of resources. It averages the costs on a large number of patients. Process costing generates less accurate cost information in comparison with job order costing, nevertheless, it produces such costing data which are judicious for fulfilling management purposes. Besides, process costing is also less expensive to obtain information (Toso, n.d.).

Standard Costing: One of the key practices used in the costing system incorporated in the healthcare organizations is standard costing. It is regarded as a prearranged estimation of what they should charge to treat a patient for a particular disease. Standard costing is developed by using the idea of actual costing and time and motion research (Toso, n.d.).

Accrual Accounting: Accrual accounting has also been developed in the area of healthcare segment. It provides a new set of information which is not available in cash based accounting system. For past few decades, accrual accounting has been represented as a reform for public healthcare segment. Moreover, accrual accounting also acts as a central aspect for budgeting in most public segment restructuring comprising healthcare (Vašiček & Roje, 2010).

Furthermore, the healthcare industry is also considering ‘Healthcare Integrated Ledger Accounting System’ (HIGLAS) a new accounting system, implemented for gaining several benefits on accounting. HIGLAS is also aimed towards the creation of a new accounting framework for the healthcare organizations for ensuring proper information in a timely manner (Shahverdian, 2013).

The prominent increase in the expenses of healthcare segment has aroused the requirement of a new accounting system to produce services in a more effective and inexpensive way. One of the significant solutions to this accounting problem for healthcare organizations is DRG which has been accepted in various hospitals. The reform in accounting in healthcare segment can provide benefit to patients as well as healthcare organizations in the form of payment and delivery methods. These accounting systems and their various practices have brought in significant changes towards international accounting practices for hospitals (Vašiček & Roje, 2010).

Nevertheless, it has been argued that healthcare service providers also must focus on the situations; standardize procedures and treatment measures in order to enhance the capability of accounting. Besides, it has also been argued that the success of operational effectives through accounting systems necessitates proper identification of cost of providing care. The new payment model of healthcare organizations has also generated arguments about measuring the total expenses of providing services. The various accounting systems comprise several inconsistencies and limitations in guaranteeing the correct and reasonable value of organizations’ financial position and performance (Vašiček & Roje, 2010).

Presently, healthcare organizations are facing conflicting interests where on one hand they require to provide quality healthcare services, on other hand they also require to ensure financial safety. In the more individual level, there are two overriding objectives of healthcare organizations where they need to achieve profitability and feasibility of the services at the same time in order to sustain. Hence, increased concentration is provided on the type of accounting system which can help to enhance the benefits from the viewpoint of profit (Finkler et al., 2011).

IV. Future Work

The future of healthcare industry lies in the use of computerized accounting system. A technology boom is currently developing which will profoundly transform the methods of delivering healthcare services. In the age of technological improvement, computerized accounting system can minimize the expenses of operational procedures. Besides, accounting systems would be more capable of transmitting huge amount of information, delivered remotely to different users. The development of accounting system is active and will change the current accounting practices over the next few decades. In future, accounting system will be able to gather huge information in order to calculate total cost of treating a specific patient. Technological development will permit healthcare organizations to deal with increasing and detailed information in an effective way. Furthermore, the procedure to implement accounting system will also change in near future as the healthcare system transforms (Seetharaman et al., 2010).

V. Conclusion

Implementation of accounting system is becoming a vital issue for the healthcare segment. This segment is presently facing constant and relentless pressure in order to satisfy the conflicting objectives, i.e. reducing the expenses without compromising the quality. With the increase of healthcare market, the accounting demand will also rise. In this context, it can be concluded that various accounting systems can be implemented by healthcare organizations in order to enhance the quality of information and as a result to increase the operational effectiveness. In addition, accounting systems can also assist in maximizing the organizational profit by eliminating unnecessary processes and providing accurate information.

References

Finkler, S. A., Ward, D. M., & Calabrese, T. (2011). Accounting fundamentals for health care management. United States: Jones & Bartlett Publishers.

Langabeer, J. R., DelliFraine, J. L., & Helton, J. R. (2010). Mixing finance and medicine: the evolution of financial practices in healthcare. Strategic Finance, 27-34.

Seetharaman, A., Raj, J. R., Saravanan, A. S. (2010). The changing role of accounting in the health care industry. Research Journal of Business Management, 4(2), 91-102.

Shahverdian, S. (2013). HIGLAS over the Years. The Centers for Medicare & Medicaid Services, 1.

Toso, M. E. (n.d.). Cost accounting and cost accounting systems in health care organizations. Retrieved from http://www.trinethealth.com/sites/default/files/Article%20-%20Cost%20Acctg%20%26%20Cost%20Acctg%20Systems%20in%20Healthcare%20Org.pdf

Vašiček, D., & Roje, G. (2010). Accounting system in Croatian public healthcare organizations: An empirical analysis. Theoretical and Applied Economics, XVII(6), 37-58.

Read

More

sponsored ads

Save Your Time for More Important Things

Let us write or edit the essay on your topic

"Accounting Systems in Healthcare"

with a personal 20% discount.

GRAB THE BEST PAPER